The big picture

Policy disruption reshapes the world order

Less than three months into Donald Trump’s presidency and the extreme policy uncertainty we wrote about in our 2025 Outlook has been even greater than we had anticipated. While the initial market reaction to the election victory was positive, the euphoria soon dissipated amid a torrent of tariffs.

President Trump’s approach to tariffs has also been chaotic. The uncertainty created could prove just as damaging, amid signs both US households and businesses are growing more cautious.

Adding to the confusion, the newly created Department for Government Efficiency has been slashing thousands of Federal jobs to root out alleged fraud and inefficiency. The blunt methods being used are creating extra uncertainty which may permeate more widely across the economy.

At the same time, we have witnessed a dramatic shift in the US’s attitude to its security role within Europe. With Europe unsure it can continue to rely on Washington, several countries, most notably Germany, are loosening fiscal policy as they look to re-arm.

The EU is to allow countries to borrow an extra €650 billion for defence. It will also provide new loans for defence procurement worth a further €150 billion.

While the global economy entered 2025 in reasonable shape, the near-term outlook has deteriorated on the back of these events. A full-blown trade war could see global economic growth of less than 2.5 per cent, which would represent one of the weakest years in decades.

However, it is possible growth could rebound thereafter (assuming the trade war does not continue to escalate) as US tax cuts kick in and as Europe ramps up defence and infrastructure spending.

Figure 1: Aviva Investors’ growth projections (per cent)

Source: Aviva Investors, Macrobond. Data as of 3 April 2025.

What this means for asset allocation

Equities

We are cautious of equities given the worsening outlook for global trade. The environment for equities is much more uncertain than in the past two years or more. There is a risk of further declines should the trade war intensify.

That said, while a weaker economic backdrop could eventually lead to a significant weakening of earnings growth, this has yet to happen. Should trade tensions begin to abate, earnings would be likely to provide support for equities.

While we proceed with more caution, we are conscious of the potential for both US tax cuts later in the year and further rate cuts from the Fed providing support to risk assets.

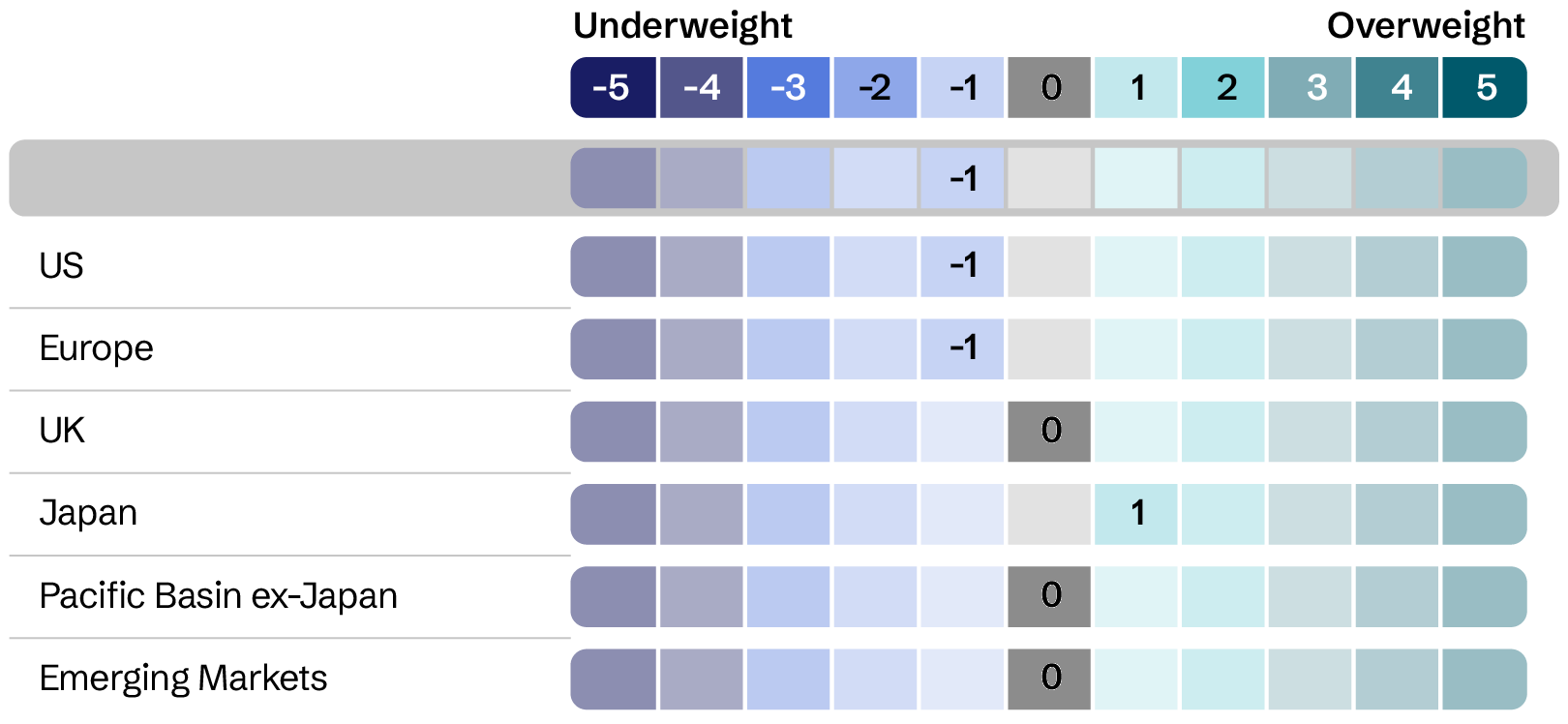

Figure 2: Asset allocation – Equities

Note: The weights in the asset allocation table only apply to a model portfolio without mandate constraints. Our House View asset allocation provides a comprehensive and forward-looking framework for discussion among the investment teams.

Source: Aviva Investors. Data as of 31 March 2025.

Government bonds

Major government bond markets have witnessed wildly different fortunes so far this year with US government debt rallying amid growing concern about the US economy and European bonds falling as investors anticipated the prospect of a sharp increase in supply.

We are overweight the US bond market. While US economic growth has been robust, recent soft economic data releases suggest the risk of a recession is rising. The imposition of tariffs raises this risk further.

As for Europe, we have seen a seismic shift in German attitudes to deficits. Together with decisions taken at the EU level, this suggests markets will have to absorb substantially increased supply over the next few years. All else equal, this is likely to translate into higher long-term bond yields.

As for the UK, we believe short-dated bonds stand to benefit from faster cuts in short-term interest rates than is currently priced into the market.

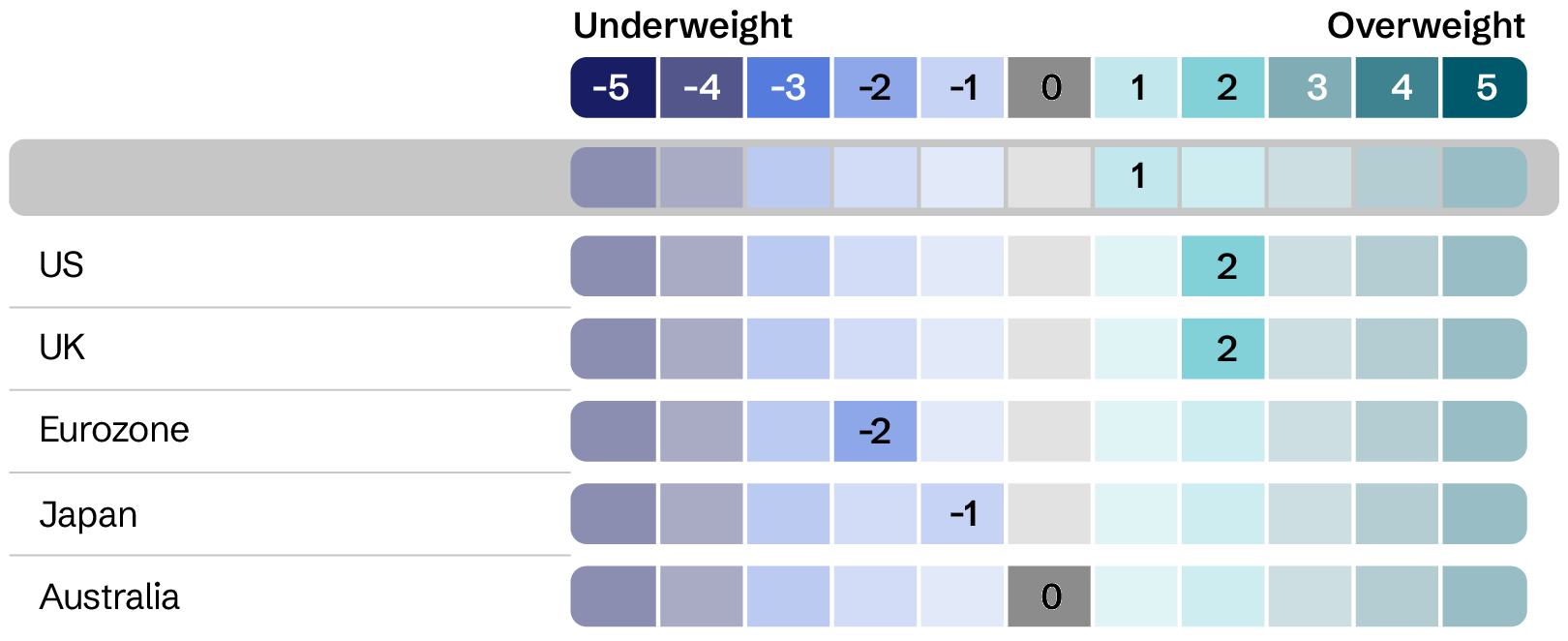

Figure 3: Asset allocation – Government bonds

Note: The weights in the asset allocation table only apply to a model portfolio without mandate constraints. Our House View asset allocation provides a comprehensive and forward-looking framework for discussion among the investment teams.

Source: Aviva Investors. Data as of 31 March 2025.

Credit

We are cautious on the prospects for corporate bonds given that the extra yield offered relative to safer government debt remains too low to compensate for the additional risk, by historical standards. We expect European investment-grade debt to outperform, while we have a preference for more defensive issues and sectors.

Our caution is partly explained by a fear that the worsening trade environment could result in a more severe economic contraction. There is a danger trade uncertainty lasts for an extended period and that US tariffs lead to tit-for-tat responses.

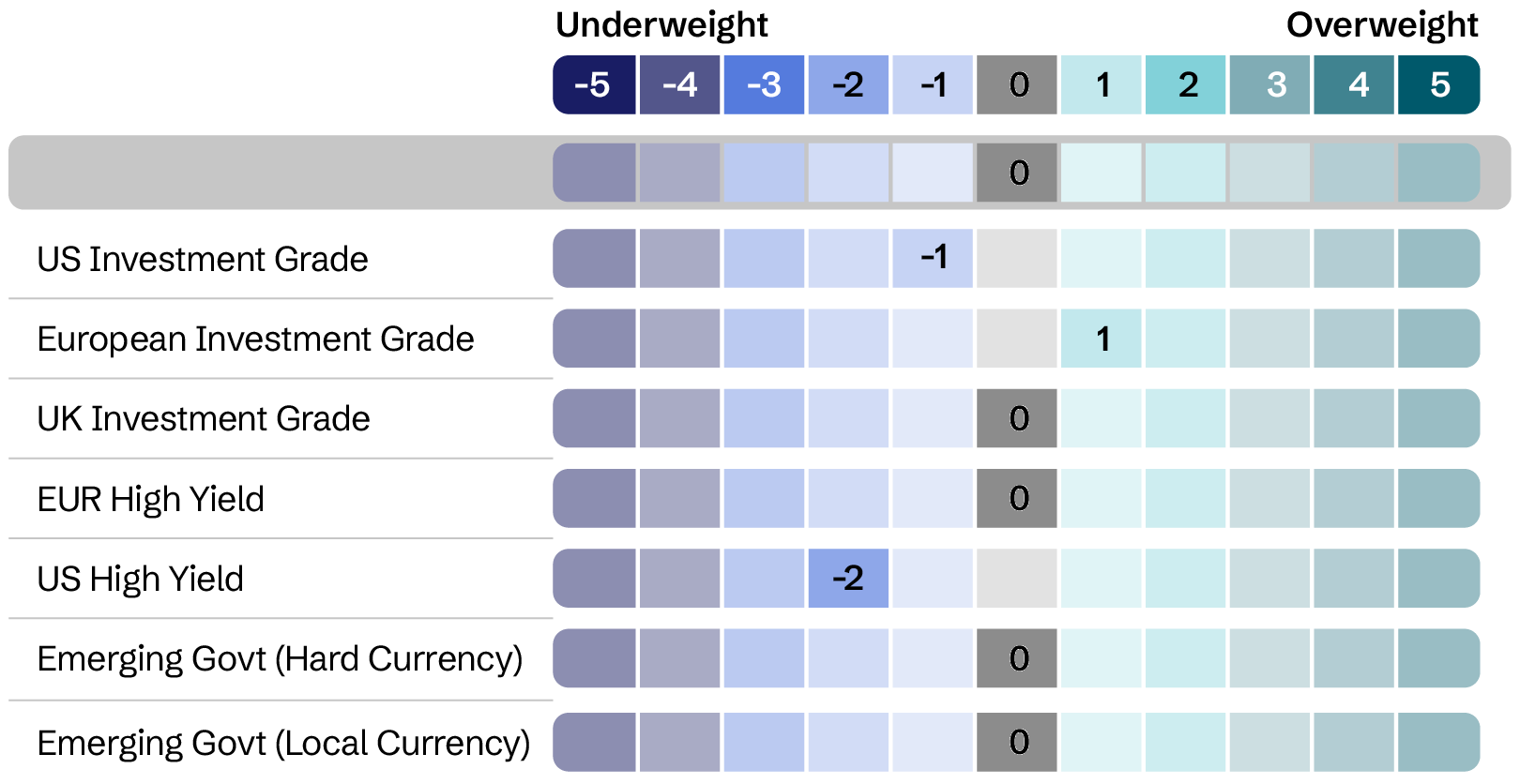

Figure 4: Asset allocation – Credit

Note: The weights in the asset allocation table only apply to a model portfolio without mandate constraints. Our House View asset allocation provides a comprehensive and forward-looking framework for discussion among the investment teams.

Source: Aviva Investors. Data as of 31 March 2025.

Four key investment themes

1. Trump 2.0: Domestic and trade disorder and disruption

The trade war has begun. While it will take time for the full impact on economies and corporate earnings to be felt, a slowdown is virtually guaranteed. The second-order impacts will include damaged consumer confidence and suspended business investment, but the severity and duration are uncertain. Countries impacted will likely retaliate.

A move toward protectionism in the US will likely alienate allies and cause damage and ‘deadweight loss’ to the US economy, while raising a modest amount of tax. This imposition of broad-based tariffs can be thought of as a negative supply shock that, when permanently imposed, raises prices and decreases an economy’s overall potential growth.

Figure 5: Effective tariff rate has risen ten-fold under the new US administration

Source: Aviva Investors, Macrobond. Data as of 3 April, 2025.

2. Solidarity and self-reliance replace the rules-based order

The reorientation of the US under its new administration, from the willingness to negotiate with the likes of Russia, to outright criticism of Europe, has prompted a re-think of many of its allies.

Many countries will look to become more self-sufficient militarily – something that the US arguably sees as a good thing. Private sector companies may also seek to terminate contracts with US firms. The biggest shift will be in Europe, where a concerted effort is being made to decrease dependence on the US, to cease internal division and infighting, and to ramp up spending to levels once perceived as fantastical.

Figure 6: Current defence spending in the EU (2024E) (per cent of current GDP)

Source: Aviva Investors, NATO, Macrobond. Data as of 31 March 2025.

3. Tech revolution’s testing times

Recent years have witnessed a boom in spending on artificial intelligence, reminiscent of the dot-com mania of the 1990s. For all the hype, we are still in the early days of this ‘gold rush’ and are seeing the first of what will doubtless be many corrections.

The inputs needed for successful models are expensive, and require huge numbers of chips and data and massive amounts of energy.

The launch of a new artificial intelligence app by DeepSeek, a Chinese AI start-up, in early 2025 was a shock for two reasons: first, American dominance was suddenly challenged, and second, the purported efficiency gain made assumptions on semiconductor demand (and profits) less certain.

But rapid technological advancement is by its very nature disruptive. Estimates of when revenues or profits will justify the hundreds of billions of investment needed vary widely. Competition will be fierce and we should expect winners and losers. Optimistic projections suggest AI-related revenues are set to surge within a couple of years. The outlook appears bright, albeit uncertain.

Figure 7: Even optimists see AI-related costs exceeding revenues for some years ($)

Source: Aviva Investors, Morgan Stanley Research. Data as of 31 March 2025.

4. Monetary divergence driven by economic variance

This theme has evolved over the past few months, as central banks that have eased monetary policy from restrictive levels turn more cautious, by-and-large ditching forward guidance in the face of uncertainty.

Core and other underlying measures of inflation have rebounded and the long-term impact of tariffs is hard to gauge. While they will tend to push up prices in the near term, their longer-term impact is less clear given the danger posed to both economic activity and individual countries’ exchange rates. Against this uncertain backdrop we see a chance for investors to unearth profitable opportunities in fixed income and currencies via relative-value trades.

Figure 8: Inflation is more stable, but above target and heterogeneous (per cent)

Source: Aviva Investors, Macrobond. Data as of 3 April 2025.

Read the House View

House View Q2 2025

Tariff turbulence, a testing time for tech, geopolitical shifts and policy divergence all feed into our asset allocation views this quarter – find out more in our latest House View.

Webcast: House View Q2 2025

Register now for our House View Q2 2025 webcast hosted by Peter Smith Senior Investment Director, with speakers Vasileios Gkionakis, Senior Economist and Harriet Ballard, Portfolio Manager as they discuss the latest economic changes impacting asset allocation.

Never miss the latest House View

Sign-up to receive quarterly emails on our collective view of global markets.

About the House View

The Aviva Investors House View document is a comprehensive compilation of views and analysis from the major investment teams.

The document is produced quarterly by our investment professionals and is overseen by the Investment Strategy team. We hold a House View Forum biannually at which the main issues and arguments are introduced, discussed and debated. The process by which the House View is constructed is a collaborative one – everyone will be aware of the main themes and key aspects of the outlook. All team members have the right to challenge and all are encouraged to do so. The aim is to ensure that all contributors are fully aware of the thoughts of everyone else and that a broad consensus can be reached across the teams on the main aspects of the report.

The House View document serves two main purposes. First, its preparation provides a comprehensive and forward-looking framework for discussion among the investment teams. Secondly, it allows us to share our thinking and explain the reasons for our economic views and investment decisions to those whom they affect.

Not everyone will agree with all assumptions made and all of the conclusions reached. No-one can predict the future perfectly. But the contents of this report represent the best collective judgement of Aviva Investors on the current and future investment environment.

House View contributors

Michael Grady

Head of Investment Strategy and Chief Economist

David Nowakowski

Senior Strategist, Multi-asset & Macro

Joao Toniato

Head of Global Equity Strategy

Vasileios Gkionakis

Senior Economist and Strategist

Important information

THIS IS A MARKETING COMMUNICATION

Except where stated as otherwise, the source of all information is Aviva Investors Global Services Limited (AIGSL). Unless stated otherwise any views and opinions are those of Aviva Investors. They should not be viewed as indicating any guarantee of return from an investment managed by Aviva Investors nor as advice of any nature. Information contained herein has been obtained from sources believed to be reliable but, has not been independently verified by Aviva Investors and is not guaranteed to be accurate. Past performance is not a guide to the future. The value of an investment and any income from it may go down as well as up and the investor may not get back the original amount invested. Nothing in this material, including any references to specific securities, assets classes and financial markets is intended to or should be construed as advice or recommendations of any nature. Some data shown are hypothetical or projected and may not come to pass as stated due to changes in market conditions and are not guarantees of future outcomes. This material is not a recommendation to sell or purchase any investment.

The information contained herein is for general guidance only. It is the responsibility of any person or persons in possession of this information to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. The information contained herein does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it would be unlawful to make such offer or solicitation.

In Europe this document is issued by Aviva Investors Luxembourg S.A. Registered Office: 2 rue du Fort Bourbon, 1st Floor, 1249 Luxembourg. Supervised by Commission de Surveillance du Secteur Financier. An Aviva company. In the UK Issued by Aviva Investors Global Services Limited. Registered in England No. 1151805. Registered Office: 80 Fenchurch Street, London EC3M 4AE. Authorised and regulated by the Financial Conduct Authority. Firm Reference No. 119178. In Switzerland, this document is issued by Aviva Investors Schweiz GmbH.

In Singapore, this material is being circulated by way of an arrangement with Aviva Investors Asia Pte. Limited (AIAPL) for distribution to institutional investors only. Please note that AIAPL does not provide any independent research or analysis in the substance or preparation of this material. Recipients of this material are to contact AIAPL in respect of any matters arising from, or in connection with, this material. AIAPL, a company incorporated under the laws of Singapore with registration number 200813519W, holds a valid Capital Markets Services Licence to carry out fund management activities issued under the Securities and Futures Act 2001 and is an Exempt Financial Adviser for the purposes of the Financial Advisers Act 2001. Registered Office: 138 Market Street, #05-01 CapitaGreen, Singapore 048946. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

In Canada and the United States, this material is issued by Aviva Investors Canada Inc. (“AIC”). AIC is registered with the Ontario Securities Commission as a commodity trading manager, exempt market dealer, portfolio manager and investment fund manager. AIC is also registered as an exempt market dealer and portfolio manager in each province and territory of Canada and may also be registered as an investment fund manager in certain other applicable provinces. In the United States, AIC is registered as investment adviser with the U.S. Securities and Exchange Commission, and as commodity trading adviser with the National Futures Association.

The name “Aviva Investors” as used in this material refers to the global organisation of affiliated asset management businesses operating under the Aviva Investors name. Each Aviva investors’ affiliate is a subsidiary of Aviva plc, a publicly- traded multi-national financial services company headquartered in the United Kingdom.